This is the official archived website of the Joint Committee of Inquiry into the Banking Crisis. It was last updated in March 2016 and will not be updated further.

Ceisteanna a Chuirtear go Minic | Teagmháil | On 27 November 2010, the Irish Government formally applied to enter a programme with the European Commission, the ECB and the IMF (also known as the Troika). This followed several weeks of informal discussions and one week of formal talks between the Government and the Troika. Entering into the Troika Programme (or “bailout” as it was more colloquially described by some witnesses) came as something of a surprise to the general public.

The Joint Committee wanted to understand why the Irish Government entered into the Troika Programme, the clear sequence of events leading to the Government decision as well as the implementation of the programme until Ireland’s exit.

The Joint Committee also sought to understand:

The question of burden-sharing, which arose in the course of the Troika Programme negotiations, is addressed in Chapter 11.

It should be noted that the ECB did not cooperate with the Banking Inquiry. While the ECB is legally accountable to the European Parliament, the Joint Committee are not aware of anything preventing the ECB from participating in a parliamentary inquiry. The Joint Committee’s efforts to engage with the ECB are set out in Volume 2 of this report.

The notion or possibility that Ireland might need external assistance at some point in managing the economic crisis was first considered by the relevant parties in September 2008. A request for “very preliminary and informal work on how a country enters an IMF programme” was requested by the then Assistant Secretary, Department of Finance, Kevin Cardiff. He said:

“Well, at that point, we might have looked for some ... we might have had to look for some external support. Certainly, it wasn’t the plan ... it was nobody’s intention but the first time I asked for some very, very preliminary and informal work on, you know, how one actually gets an IMF programme, was in September 2008, and at that point, I was thinking, you know, there was no work done on it. I just asked a colleague to make a discreet inquiry as to how you get into these things, if you do need them, just as a precaution because things were very bad from then.”1

In 2009 and again in 2010, it was communicated to the Government that IMF assistance was available, if needed. Former Deputy Director, IMF, Ajai Chopra, stated in evidence that the IMF had been in formal contact with the Irish authorities on at least two different occasions, in 2009 and 2010. However, he said this should not be interpreted as giving the impression that the IMF “were out here badgering the authorities to get into a programme…”2

If the IMF was not “badgering” the Government, neither were the Irish authorities engaging with the suggestion. As Kevin Cardiff said:

“Then in 2009, I believe there were hints in Washington, possibly also in Dublin, that, you know, IMF would be available if we wanted them. At that point, the Minister gave a pretty firm instruction to me and to others that we were not engaging with that suggestion but in part because ... remember, a bank crisis means you have to fill gaps in liquidity and gaps in bank liquidity are enormous. Capital is a lesser problem; liquidity is an enormous gap. And you really need the firepower of a central bank to do that. Now, in 2009 and into 2010, we had no problem getting funds for the Government, which is what the IMF provides.”3

However, the consideration of entering a programme was not just an economic one; being “bailed out” had broader implications for the country, as former Chief Executive, NTMA, Michael Somers captured in his testimony before the Joint Committee:

“I never thought that it would happen. I mean, one of the nightmares for us for many years – because I was responsible for our end for many years – was the IMF. I mean, that was the thing. Actually … because we would be writing memos to Government telling them to cut back on their expenditure. That was the bogeyman that we held up, “Listen, if you don’t behave yourselves and get your finances under control, the next thing is we’ll have the IMF in here running the show for us.” So, for me, I felt it was the ultimate humiliation actually for us, as a country, to have the IMF come in to run the show for us.”4

Ajai Chopra told the Joint Committee of the “stigma” associated with entering an IMF programme:

“…the right time for a country to enter into a programme is when it’s vulnerable but not in a full-blown crisis. Now, within that, there’s a continuum. At one end of the continuum, you have a situation where a country can ask for help at the very first sign of some trouble, or it could wait, and the other end of the continuum would be that it cannot pay next week’s wages, pensions and debt service. So within that, there’s a number of other possibilities. Now, it’s most unusual for a country to come right at the beginning, at the first sign of trouble, because there is an enormous amount of stigma. ... It’s well known that there’s stigma about entering into an IMF programme. And also there’s always the hope that you can ride out the troubles. But it’s equally disadvantageous to come at the very end, and Ireland did not do that.”5

Possibly the most active suggestion on the part of the IMF was that the Irish authorities might consider a programme of assistance came in the second quarter of 2010. Former Governor of the Central Bank, Patrick Honohan, spoke about this in his evidence to the Joint Committee:

“So I got a call from Ashoka Mody, who we know was subsequently in here and he ... out of the blue he said “You know we’re coming, we’re coming later in the month for the Article 4.” Yes I know. “And we’re just wondering would you think Ireland would be interested in one of these precautionary programmes?” And I knew that ... there are a number of ... two particular precautionary programmes, I’m not sure which one he was talking about. One of them was for countries that were really considered very well run, very well managed but just vulnerable to pressure from the market. Mexico I think qualified for one of these and may have taken one of these ones.”6

The Central Bank was not advocating that Ireland pursue a precautionary line from the IMF at this stage. Patrick Honohan said:

“And I thought this might be quite good, we’d get a ... we’d get a seal of approval, potential access to money and it might be good. But I didn’t think it as a wonderful thing which would have really been, you know, let’s go for that, because if I had, we would have been advocating it as well.”7

Nevertheless, Patrick Honohan said that he thought the idea worth considering:

“In six months’ time, we had a real line [bailout programme]. So it ... okay, the step I took was to tell Mody, “I think you should raise it with the Government because I think it’s a good idea.” He raised it, I presume ... well, I know, because they came back to me and it was shot down. But I think it was ... it’s more that it reflects, first of all, a sense that the IMF team thought we were being well-run, because they didn’t give these things to countries that were not being well-run, and that there was that sense of concern. We weren’t there blithely going along saying, “Everything’s fine here.” We were aware of the concern.”8

Developments in Greece around this time may present some context. In April 2010, Greece was in discussions to enter a Troika Programme. Former Taoiseach Brian Cowen, told us that international perceptions of Ireland “were not helped” by the Greek situation whereby: “Greek Government bond yields [had] soared to over 15% … its Government could not borrow any further [and] it applied for external assistance in April 2010…”9

The Greek request for assistance prompted the suggestion by Patrick Honohan of the Central Bank that Ireland “could” be next to request assistance. As he told the Joint Committee, referring to an interaction he had with the then Minister for Finance, Brian Lenihan:

“[Brian Lenihan:] I have to ask you your advice on whether we should go ahead and support and put Irish money into this Greek programme that’s being envisaged.” So I think it was 10 April and I said, “I think you should,’’ and he said, “Yes, I have the same view because you know we are going to make money on it because we are borrowing at this and we are going to get this amount of money’’, and I said, “That’s not the reason,’’ I said, “The reason is we could be next.’’ “Oh no,’’ he said, “No, no, I’ve been talking to the people in Brussels and they say Portugal is next.”10

It is important to underline the seriousness of the situation facing the Irish Government through 2010. As Brian Cowen said:

“But the point I’m making to you is that, regardless of what the IMF were saying, you know, we were coming to a position in relation to our own situation to say that we would prepare a four-year plan anyway, regardless if there was never a European dimension to it.”11

Sovereign deficits were climbing in Europe as the crisis continued and the possibility of a Eurozone country exiting the Euro, either in tandem with or because of a default on Sovereign debts, was being discussed openly.

Kevin Cardiff spoke about the work of a small group focusing on Ireland’s potential exit from the Euro:

“There was certainly work done on what would happen if we found ourselves unceremoniously shown the door or if that became the only option” before continuing: “there was a number of contingency papers drafted but the work was kept to an absolute very small group of people,”12 and “the policy was clear… it was ... the Minister’s view that the Government’s view was clear. We are not working towards exiting the euro; we were working towards staying in it. That was always clear; there was never a debate.”13

As already set out in Chapter 7, the Government decided in September 2008 to guarantee all liabilities, both existing and new, for each of the Covered Institutions (the State Guarantee). Under the Credit Institutions Financial Support Act 2008 (CIFS Act 2008) all deposits, senior debt, covered bonds and dated subordinated bonds of the Participating Institutions were covered under this blanket guarantee scheme up to 29 September 2010. The only major exclusion was perpetual bonds.14

Within the two year period of the State Guarantee, the Irish Covered Institutions were able to refinance liquidity requirements as they were supported by the State’s Guarantee and had access to monetary authorities. Initially the CIFS scheme guaranteed €375.25 billion, the additional €77.41 billion was already covered by the Deposit Guarantee Scheme.15 The European Commission in its ex post evaluation of Ireland’s bailout programme included the following assessment of the linkage that had become established between bank debt and national debt:

“In practice in September 2008, the authorities issued a two-year guarantee on existing banks’ liabilities (Credit Institutions Financial Support Scheme - CIFS) amounting to €375bn (200% of GDP), in order to overcome banks’ funding problems and address potential capital shortfalls. As a result, the solvency of the Irish sovereign and that of the banking system became directly intertwined. This eventually turned the banking crisis into a sovereign debt crisis…”16

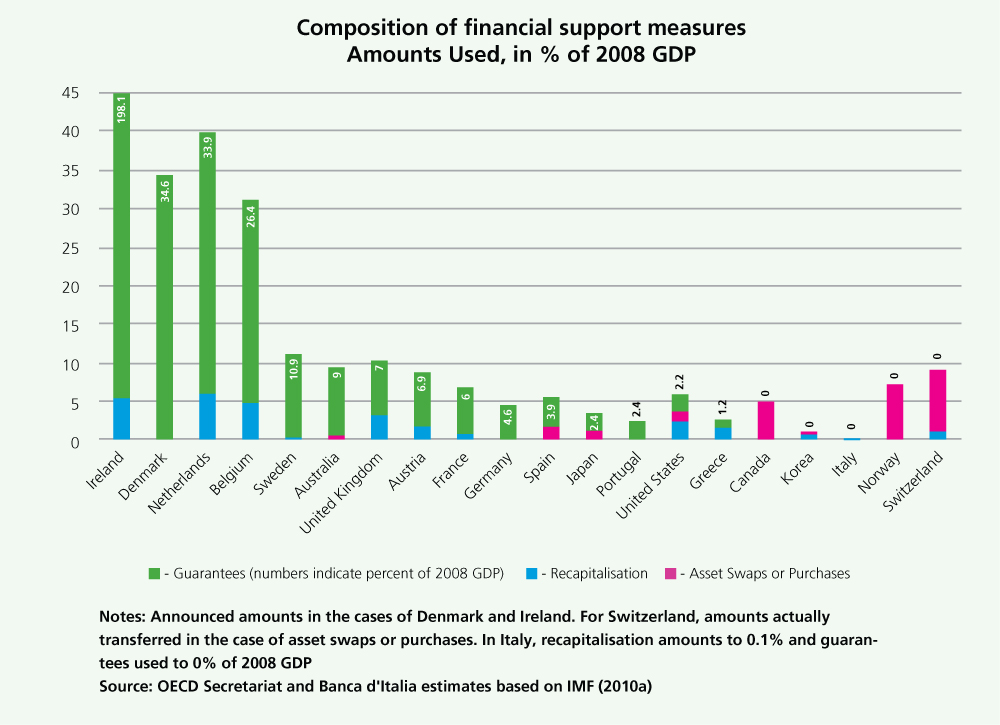

Source: Extract from OECD journal financial market trends volume 2010 Figure 7.1

As illustrated above, Ireland had by far the highest level of guaranteed financial support provided in % of GDP in 2008.17

This increasing volume of bonds, maturing in September 2010, created a potential “ funding cliff ” in the eyes of the authorities.

Author and journalist, Simon Carswell said that, because of the nature of the State Guarantee, “there was always going to be a funding cliff at a particular point”.18

Patrick Honohan told us: “if it had have been a one-year guarantee, the cliff would have just come earlier” .19

In early 2010, the Central Bank, through the Prudential Capital Adequacy Review (PCAR) process, identified an additional need for approximately €10.9 billion in capital requirements for the Covered Institutions. As NAMA continued its work in transferring loans from the Covered Institutions and the extent of the discounts became clear, capital requirements for some of the banks increased (see Chapter 8).

Between October 2008 and May 2010, the Covered Institutions issued 174 guaranteed bonds, the total value of which amounted to €61.2 billion or, on average, €400 million per issue, as per the following table.